{kind=link}

Ever since the housing crisis in 2009, getting approved for a loan while being self-employed was instantly more difficult than for a W2 Salaried borrower. Fortunately, lending and credit standards have loosened but far from the pre-2008 days of when your pet could be approved for a no doc mortgage.

In 2019, more and more self-employed borrowers who receive a 1099 or own their own business have better options to obtain a home loan. Nowadays, there’s loans that do not require two years of tax returns with just 10-percent down if your credit report is acceptable.

However, the differences in the rate and fees is significant and a reason you may want to do all you can to give the lender your most recent two year of tax returns.

Example of a Recent Borrower:

He needed to refinance his home to remove an ex-spouse from a recent divorce and take out some cash for miscellaneous expenses.

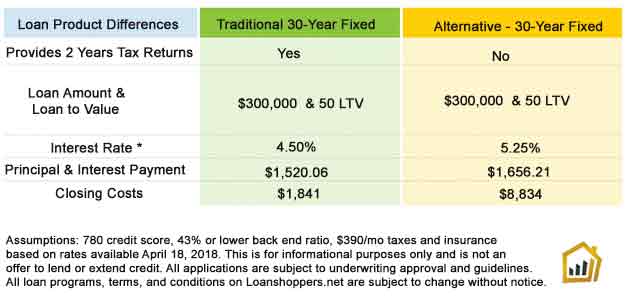

Loan amount: $300,000

Estimate home value: $610,000

Property taxes & insurance: $390/month

Credit scores: over 780

Occupation: business owner

Gross Income: $110,000

His dilemma was he deducts a lot of valid expenses from his business reducing his adjusted gross income (AGI) to around $55,000.

Fortunately, he had no other monthly debts such as a car payment, credit card or student loan debts.

He was adamant on using the bank statement mortgage since it did not require any tax returns. This would show his true gross income.

Interest Rate Differences

The rate he would get at the time is 5.25% on a 30-year fixed. That’s not bad at all but when you consider he is being forced to refinance from his current 3.875% fixed mortgage just to remove an ex-spouse, it doesn’t sound so great.

If he could provide his IRS 1040s and all schedules he would qualify for a 30-year fixed rate at 4.50% which is a very good improvement.

$1,656.61 – 5.25% (30 year fixed with 12 months of personal bank statements)

$1,520.06 – 4.50% (30 year fixed with 2 years of tax returns)

The difference over seven years which is when most people sell their home or refinance is $11,424. If he were to keep the mortgage for the full 30 years, he would pay an additional $48,960.

If his credit scores were below 720, the rate & payment difference would be even more dramatic.

Closing Costs Differences

The differences became larger when you factor in the fees associated with a bank statement loan vs. a conventional 30-year fixed.

The fees for the traditional loan had no points. The closing costs total came out to $1,841, with $1,051 being applied to prepaid interest, taxes and insurance. In addition, the net cash back to him was approximately, $26,000.

The fees for the bank statement loan were $8,834 (almost 5 times the traditional loan), with $4,135 applied to prepaid interest taxes and insurance.

Because he had very little monthly debts, his tax deductions actually did not affect him in qualifying for a traditional mortgage using two-years of tax returns. He only needed to make $4,244 month to qualify.

$1,520 – Principal & interest payment on new 30 year fixed at 4.50%

+

$390 – (Property taxes and insurance)

TOTAL: $1,910 ( P.I.T.I)

$1,910 / .45 = $4,244

Therefore, if his previous two years of tax returns showed an adjusted gross income (AGI) of $50,920 he can accomplish what he set out to do. He’ll get a lower rate and much lower fees than anticipated.

While it’s true the bank statement mortgage can help lots of borrowers it may not always be the best option. Let your loan officer know what your AGI is to make sure you are getting the best available loan choice.